India’s Challenges After Independence and Its Movement Towards Modernization

After achieving independence in 1947, India adopted a mixed economy model with elements of both socialism and capitalism, aiming for rapid industrialization and self-reliance.

Early Challenges (Pre-1991 Era)

The sources detail several significant challenges that resulted in slow economic growth for decades:

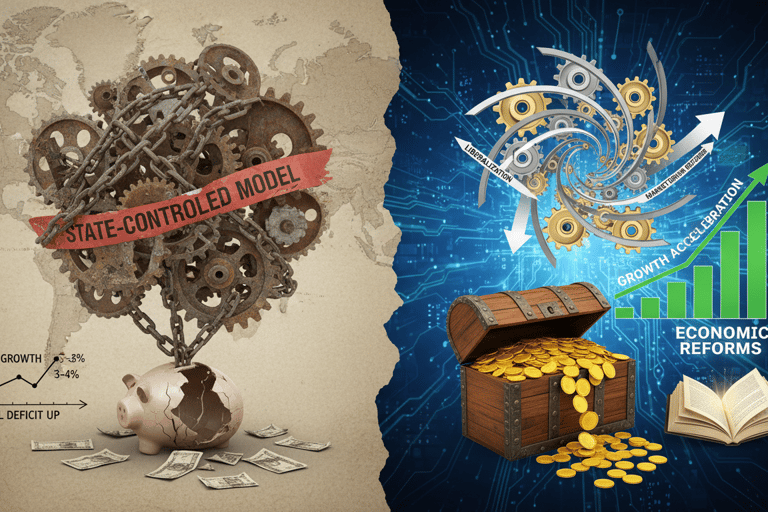

1. State-Led Economic Model: India pursued a "dirigiste model," which emphasized state control of key industries like banking, insurance, and heavy industry, along with policies promoting import substitution. The early planners, including Prime Minister Jawaharlal Nehru, reportedly did not trust private entrepreneurs, leaving the state to act as the primary entrepreneur, which ultimately failed to create an industrial revolution.

2. The "License Raj" and Regulation: The industrial sector was severely regulated by the "License Raj," a system that required businesses to obtain numerous permits to start and operate. These rigid controls discouraged new industries, fostered monopolies, and led to the proliferation of uneconomic-size plants in uncompetitive locations using inferior technology.

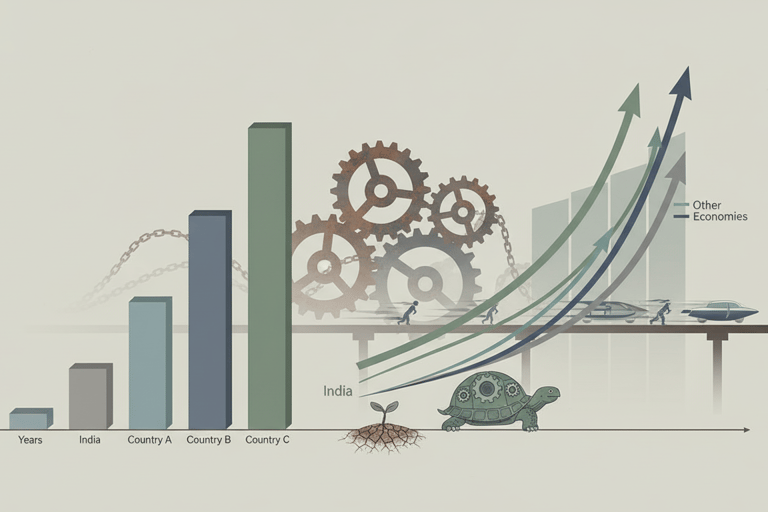

3. Slow Growth Rate: Prior to 1991, India’s GDP growth rate was sluggish, averaging around 3–4% per year. India’s slow growth rate compared poorly to other developing countries, such as Pakistan (5%), Indonesia (6%), Thailand (7%), Taiwan (8%), and South Korea (9%).

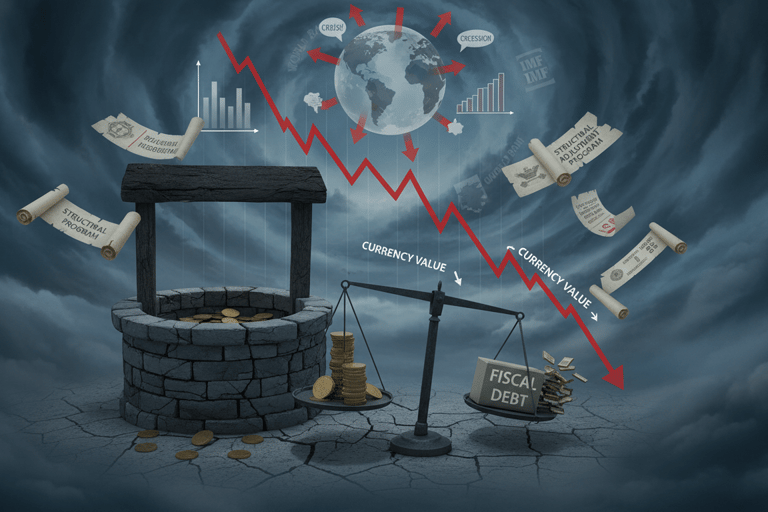

4. External and Fiscal Crises: India's fixed exchange rates led to foreign exchange reserves being depleted to maintain parity, and by the late 1980s, the fiscal deficit had reached over 8% of GDP. This culminated in a severe balance of payments crisis in 1991, where foreign exchange reserves fell to dangerously low levels, covering less than three weeks of imports. India was forced to seek assistance from the International Monetary Fund (IMF) and the World Bank, who made financial support conditional on implementing structural adjustment programs.

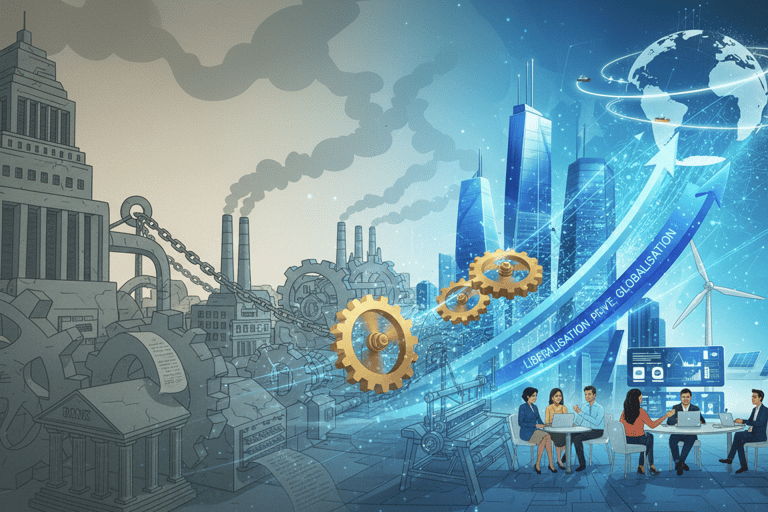

The 1991 crisis forced the government to initiate a comprehensive reform agenda known as Liberalisation, Privatisation, and Globalisation (LPG). This marked a turning point, fundamentally altering India's economic landscape.

Key aspects of India’s modernization include:

Accelerated Movement Towards Modernization (Post-1991)

Dismantling Controls: Liberalization largely abolished the License Raj for most industries (except for 18 strategic and security-related sectors). It also scrapped the policy of government approval for foreign technology agreements to incentivize technological advancement.

FDI and Growth Boost: Reforms led to an increase in foreign investment, a reduction in crony capitalism, and a shift toward a market-driven economy. Foreign investment increased by 316.9% between 1992 and 2005, and India’s GDP grew significantly. Post-1991, GDP growth rates often exceeded 6–7%.

Services Sector Dominance: The reforms spurred the exponential growth of India’s IT and services sector, making India a global hub for software services and outsourcing. The services sector now accounts for over 50% of India’s GDP.

Continued Reforms and Infrastructure: Modernization efforts continue through strategic policies, such as:The Insolvency and Bankruptcy Code (IBC) of 2016, which aimed to expedite resolution of distressed assets and improve India's credit culture. The Goods and Services Tax (GST), implemented in 2017, unified multiple indirect taxes into a single framework, promoting a common national market, increasing transparency, and formalizing the economy. GST has contributed to productivity improvement in logistics and transport. Infrastructure Investment has been prioritized, exemplified by projects like the Golden Quadrilateral (GQ), which upgraded key highway networks, resulting in increased manufacturing activity and improved efficiency. Total infrastructure spending has increased exponentially, with budget allocations rising to ₹10 lakh crore in 2023-24. The Production Linked Incentive (PLI) Scheme (launched 2020) aims to accelerate industrial growth, generating substantial production value (₹12.50 lakh crore as of August 2024) and positioning India as a global manufacturing hub.

Social Progress: India has demonstrated sustained progress in human development, with its Human Development Index (HDI) ranking rising to 130 out of 193 countries in 2023. Life expectancy has reached its highest recorded level for the country, at 72.0 years.

Join us in sustainable innovation efforts.

Engage

Support

© Donghaeng-manthan 2025. All rights reserved.